by JoAnna Billete, CPA

Introduction

You’ve probably heard of the 50-30-20 budgeting rule—it’s everywhere these days! But is it really as simple as it sounds? The short answer: yes, but with a twist. This guide will not only explain the rule but also show you how to adapt it to your life and start building a budget that works for you.

What’s the 50-30-20 Rule All About?

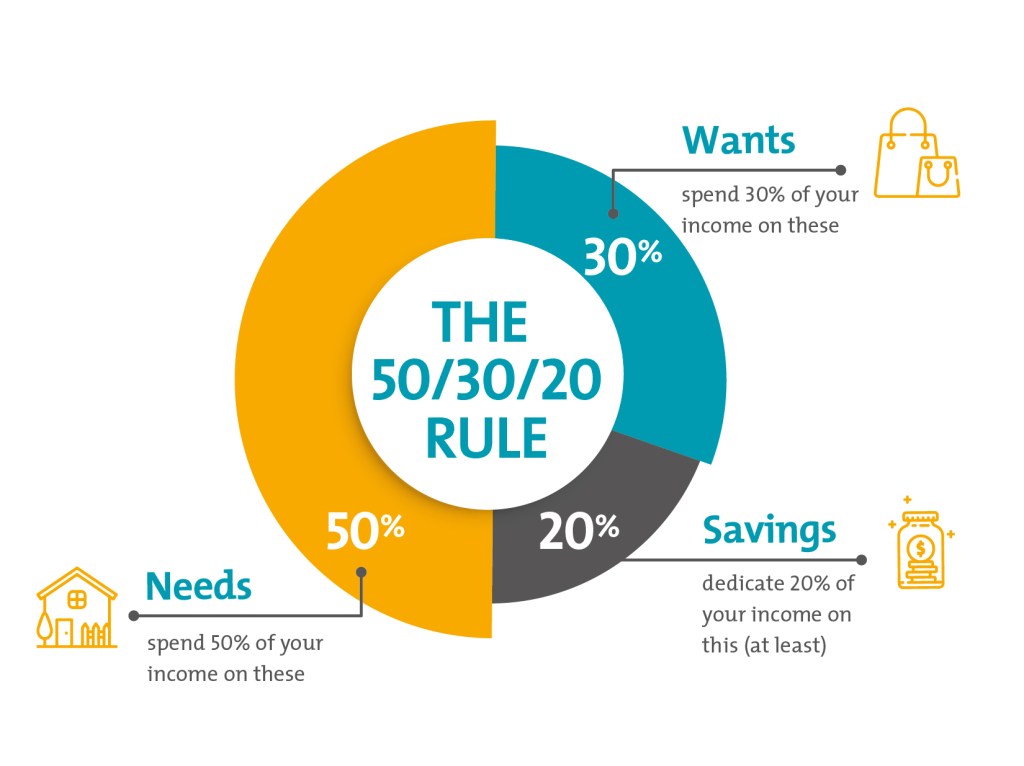

At its core, the 50-30-20 rule helps you manage your money by dividing it into three categories:

- Needs (50%): Essential expenses like rent, utilities, groceries, and transportation.

- Wants (30%): Fun, non-essentials like dining out, hobbies, and entertainment.

- Savings and Debts (20%): Building your future through emergency funds, debt repayment, and investments.

Think of your income as a pie, with three slices. Each slice has its purpose, but you can tweak the recipe to suit your life.

How to Make the 50-30-20 Rule Work for YOU

Meet Sarah

Sarah earns $4,000 per month. Here’s how she uses the 50-30-20 rule:

- $2,000 goes to rent, groceries, and bills (50%).

- $1,200 is for fun—like dining out and hobbies (30%).

- $800 is saved for emergencies and paying off her student loans (20%).

Sarah’s breakdown works because it aligns with her priorities. But what if your situation is different? Here’s how to adjust:

- High Debt? Dedicate more than 20% to paying it off and reduce the “wants” category temporarily.

- Big Goals? Saving for a down payment? Cut back on wants to boost savings.

Breaking Down Needs vs. Wants

This is where most people get tripped up. Ask yourself:

- Is it essential? Would life come to a halt without it?

- Does it align with my goals? Will this help me get closer to financial stability?

Pro Tip: Track your spending for a month and categorize every expense as “need” or “want.” Be honest—does your daily coffee run really belong in “needs”?

Budgeting Challenges and Simple Solutions

- Impulse Buying

- Solution: Use the 7-Day Rule. Wait a week before purchasing non-essentials. You might find you don’t need them after all!

- Sticking to Savings

- Solution: Automate it! Set up recurring transfers to your savings account so the money is gone before you can spend it.

- Unexpected Expenses

- Solution: Build an emergency fund with 3–6 months’ worth of expenses. This cushion keeps you from relying on credit cards for surprise costs.

Tools to Make Budgeting Easy

Apps: Use tools like Mint, YNAB, or PocketGuard to track spending and automate savings.

Spreadsheets: Prefer manual tracking? A simple spreadsheet can work wonders.

Pen & Paper: For the old-school budgeters, writing things down is just as effective.

Visualizing Your Budget

Here’s a quick visual of how the 50-30-20 breakdown looks for someone earning $4,000 a month:

- Needs: $2,000

- Wants: $1,200

- Savings/Debts: $800

Image courtesy of Infinity Financial Solutions

FAQs About the 50-30-20 Rule

Q: What if my income is inconsistent?

Use your average monthly income over the past year as your baseline. During high-income months, allocate more to savings to cover leaner times.

Q: Can I adjust the percentages?

Absolutely. The rule is a guide, not a law. Adapt it to fit your life and financial goals.

Q: How do I handle irregular expenses?

Plan ahead by creating sinking funds for annual costs like car insurance or holiday gifts.

Take Control of Your Money

Budgeting isn’t about deprivation—it’s about balance. The 50-30-20 rule provides a simple starting point, but the key is tailoring it to your needs and goals.

Ask yourself today:

What’s one small step I can take to start my financial journey?

Share your thoughts and experiences in the comments below—we’d love to hear them!

Prefer to listen instead? Check out the audio version of this post:

🎧 Listen on Spotify

📺 Watch on YouTube

Leave a comment